Have you recently found yourself drowning in auto loans, student loans, and credit card debt? You’re not alone. Millions of American consumers are having trouble with paying their monthly credit card bills because they’ve gotten overextended, recently lost their job, or had to take care of another financial emergency. Weighing the pros and cons of loan consolidation is essential before making a commitment to paying off your credit cards using a method like debt consolidation.

The Pros of Debt Consolidation

Depending on your situation, there are a variety of ways to consolidate your credit card bills and other loans. Some of the ways including using the equity in your house, calling a third party organization to help you with payments, and taking out a personal loan to pay off your entire credit card balance.

- Using a home equity loan – The major benefit to taking out a home equity loan for consolidation is that you’ll save money with lower rates. You might be able to deduct the interest you pay on the loan as well.

- Using a debt consolidation firm – Debt firms work by allowing them to negotiate with your credit card companies, and then paying them directly. This is an easy way to consolidate your debt because you won’t have to worry about making monthly payments to multiple creditors. Before you hire a consolidation company, use a loan calculator to compare the fees being charged by the firm against the interest rate you could get with a personal loan.

- Using a personal loan – A personal loan is a great way to pay off credit card debt because you’ll be able to save money with interest rates. Credit card interest rates are always high, unless you pay the balance off in full. This option also allows you to make one low monthly payment instead of multiple payments to different companies.

Generally speaking, if you have serious trouble with credit card debt, consolidation is a great option. If you have less than perfect credit and you don’t own a home, you can still use a consolidation firm to help you pay off the debt or ask a friend or family member for a personal loan. If paying back a friend or family member requires you to include interest, use a loan calculator first to determine if the option still suits you.

The Cons of Debt Consolidation

If you have a poor payment history with your credit cards, consolidation may not be the best option for you.

- Using a home equity loan – When you take out a home equity loan, you’re putting your home on the line for your credit card debt. If you’ve had trouble paying your bills in the past, this is not a good option for you.

- Using a third party consolidation firm – You have to be careful when talking to firms over the phone. Many of these companies charge outrageous fees to help you with your debt and the payments can be enormous. Use a debt consolidation calculator first to determine the overall cost when choosing this option.

- Using a personal loan – If you can’t pay the money back, your credit or your relationships with friends and family who gave you the money will be ruined. Even asking for the money from someone you know can be embarrassing. Use this as a last resort, if at all.

Being able to pay your bills on time is an essential factor in all three options. If you weren’t able to pay your credit card bills on time because of lack of financial planning, consolidation may not be for you.

Alternatives to Debt Consolidation

Consolidation can be a huge financial and psychological burden. To avoid the unwanted stress, consider the following alternatives:

- Negotiate interest rates – If you feel like you can still keep your credit cards open but want to reduce the amount of debt you have now, try to negotiate the interest you pay on each card. If you’ve been an exceptional customer and have paid your bill on time, the company might be willing to cut you a deal.

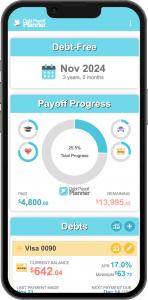

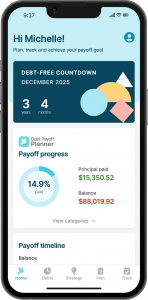

- Debt payoff planner – Use a planner to make an aggressive plan to pay off your debts. Depending on how much credit card debt you have, this can take several months or years, but doubling or tripling your credit card payments and reducing other non-essential expenses can be a rewarding experience in the end.

- Debt settlement – Calling your credit card companies and asking for a settlement is the best place to start. It doesn’t hurt, and many financial companies will consider it if you close the credit card account first. This option won’t work with all loan consolidation issues, but for serious cases it may be a viable option.

Summary

Each option requires a significant amount of research and planning. Regardless of whether you choose to consolidate your debt yourself or get help from a debt consolidation firm, be sure and use a debt payoff calculator and track where you are at all times. In some cases, if you need both loan consolidation and credit card consolidation, two different methods of repayment will be necessary.

There will be unpleasant times ahead for sure. Paying off debt is an emotionally taxing process, and at first it will feel overwhelming. Just remember this: The best time to start was a year ago. The next best time is today.

Photos by Quazie.